Democratic Presidential hopeful Hillary Clinton botched her debate question on her longstanding ties to Wall Street and her reliance on their campaign donations.

CLINTON: So I represented New York, and I represented New York on 9/11 when we were attacked. Where were we attacked? We were attacked in downtown Manhattan where Wall Street is. I did spend a whole lot of time and effort helping them rebuild. That was good for New York. It was good for the economy, and it was a way to rebuke the terrorists who had attacked our country.

The reaction to Hillary's wrapping her ties to the greed and leverage boys in a 9-11 flag was swift.

WaPo reported:

Wall Street is not a warm and fuzzy friend in need of comfort in the

minds Americans still digging themselves out from the Great Recession

and monstrous housing crisis.

... just the day before Saturday's debate, millions of Americans watched in

horror as France, this country's first ally, endured its own large-scale

terrorist attack. Especially in this context, it was not -- and on this

there really is little room for debate -- appropriate to summon the

memories of 9/11 or the fallout from a terrorist attack to explain her

connections to Wall Street and its campaign cash.

A week after the debate

NYT ran a piece on Hillary's Wall Street "image problem." This piece made no mention of The Clinton Foundation, which employs similar methods as Wall Street by raising and accounting for funds.

NYT did not mention the Clinton Foundation

having to refile years of tax returns with the IRS for omitting donations from foreign governments, some unauthorized, while Hillary served as Secretary of State. The Clinton's

skirted the agreement that allowed the foundation to keep raising money from foreign governments and circumvented the ethics procedure within the State Department for approving

Bill Clinton's speeches.

The Clinton Foundation also funnels donor money to

friends and insiders.

And efforts to insulate the foundation from potential conflicts have

highlighted just how difficult it can be to disentangle the Clintons’

charity work from Mr. Clinton’s moneymaking ventures and Mrs. Clinton’s

political future.

Fall 2013 saw Hillary move into offices at the foundation’s new headquarters in Midtown Manhattan, occupying two floors of the Time-Life Building. Hillary is in

close proximity to Wall Street.

The foundation, which has 350 employees in 180 countries, remains

largely powered by Mr. Clinton’s global celebrity and his ability to

connect corporate executives, A-listers and government officials.

Recent

revelations show The Clinton Foundation a 50% owner and sole manager of a $20 million South American private equity firm, Acceso. The Clinton Foundation holds an equity stake in two Colombian companies, Alimentos SAS and Fontel SA.

Many of the Clintons' speeches the last decade have been to private equity audiences. Bill Clinton advised Ron Burkle's Yucaipa and Teneo. Chelsea worked for Avenue Capital and sits on the IAC board. Hillary

spoke to numerous PEUs after retiring from public service.

The Clintons are Wall Street, plain and simple. It's not an image. It's a fact.

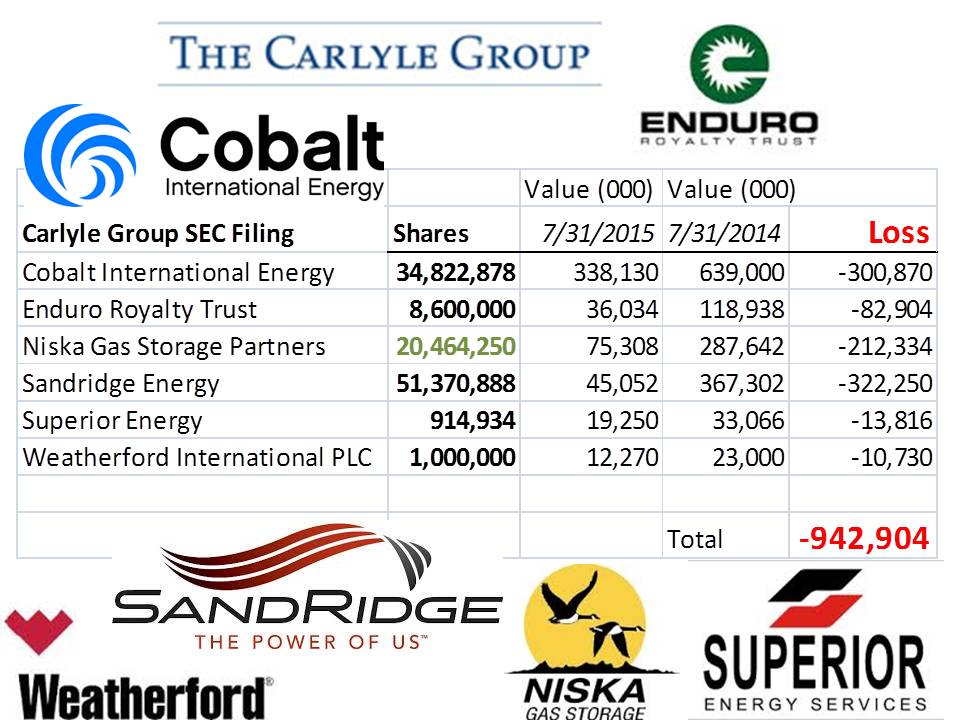

Note: PEUReport found an

undeclared speech Bill Clinton gave to The Carlyle Group and has

numerous posts on the Clinton Foundation.